In an era of profound fragmentation, these have stayed the same

Supermarket employees across the organization, from the C-suite to the checkout, spend an enormous amount of time thinking about a veritable galaxy of products.

Consumers don’t.

That may be one of the most important insights to come out of McKinsey & Company’s State of Grocery North America 2026 report.

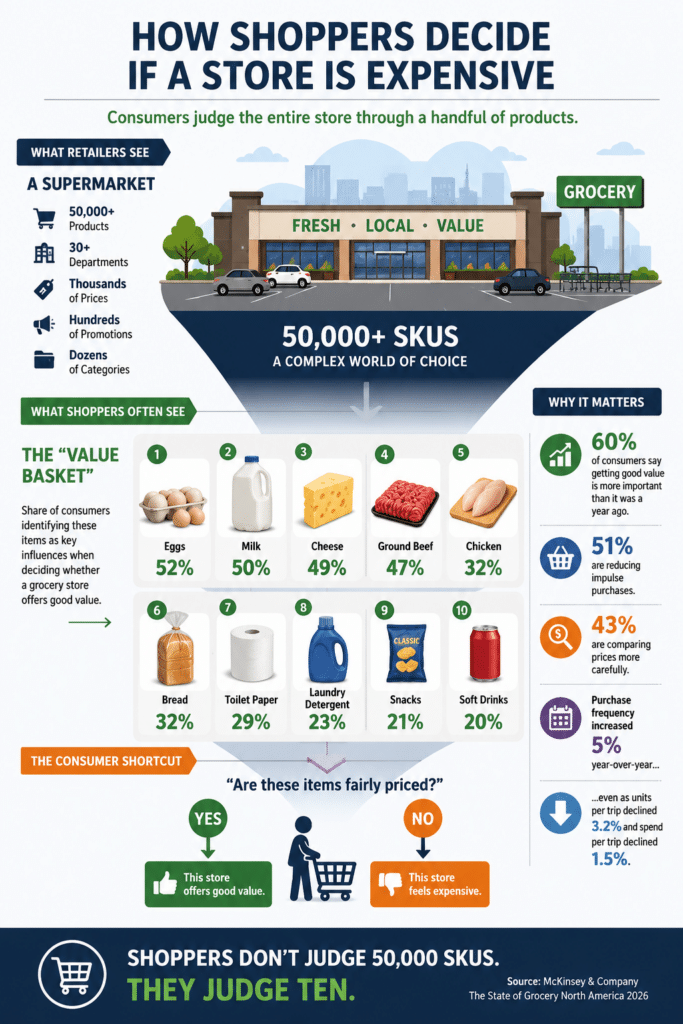

While the average North American supermarket carries anywhere from 30,000 to 60,000 SKUs, shoppers often form their opinion of a store’s value proposition based on an almost astonishingly small set of products.

According to McKinsey, these are: eggs, milk, cheese, chicken, ground beef, bread, toilet paper, snacks, laundry detergent, and soft drinks.

That’s it. Those are some of the most influential items consumers use when deciding whether a retailer offers “good value.” Eggs alone were cited by 52% of consumers, followed by milk at 50%, cheese at 49%, ground beef at 47%, and chicken at 32%.

Fail to convince customers here, and you’ll likely fail to keep their business.

It shouldn’t come as a surprise that your average customer hasn’t conducted a comprehensive audit of the store. They use shortcuts.

That “shortcut” behavior is becoming more and more important because shoppers remain intensely focused on value. McKinsey found that 60% of consumers say “getting good value” has become more important than it was a year ago. More than half (51%) report reducing impulse purchases, while nearly half (47%) say they are buying more private-label products. Another 43% report relying more heavily on promotions, while 43% are comparing prices more carefully than before.

So, clearly consumers are paying attention – just not to everything.

The report also shows that shopping behavior itself is changing. Grocery purchase frequency increased 5% year over year between August 2024 and August 2025, even as units per trip fell 3.2% and spend per trip declined 1.5%. McKinsey’s numbers show shoppers are making more trips but buying less on each visit.

So it follows that, if shoppers are making smaller, more frequent trips, they are repeatedly coming across the same highly visible products – and their price tags.

Eggs… Milk… Bread… Chicken… Ground Beef…

That’s how the products consumers purchase most often become the products that shape their overall judgement on the value proposition on offer.

The grocery industry has long referred to these categories as key value items, or KVIs.

What’s striking in McKinsey’s findings is just how concentrated and strong those perceptions remain in an era when just about everything is fragmenting. Despite the explosion of private label, e-commerce, retail media and personalized promotions, consumers still rely on a handful of everyday staples when deciding whether a retailer offers good value.

The best retailers understand this. In fact, 81% of grocers McKinsey surveyed said they expect to place greater emphasis on KVIs in their promotional strategies over the next two to three years.

If the KVIs are staying more or less the same, the report suggests that value itself is evolving. Rather than competing through blanket price reductions, grocers are increasingly building integrated value systems that connect pricing, promotions, loyalty, personalization and private brands. McKinsey found that 88% of grocers expect greater integration between promotions and loyalty programs, 88% anticipate more targeted offers, and 84% expect more personalized offers in the coming years. Meanwhile, the share of promotions that are fully personalized is expected to jump from 35% today to 55% within the two to three year timeframe of the survey.

Yet amid all that sophistication, consumers appear to be asking for something simpler.

But… Will Customers Like It?

Fully 71% of consumer respondents say they prefer lower, more consistent everyday pricing over a system built around frequent promotions and higher base prices. EDLP, anyone?

That statistic should positively reverberate throughout the industry.

For years, retailers have invested heavily in increasingly complex promotional ecosystems. But shoppers continue to evaluate value in surprisingly straightforward ways. They look at the products they buy most often.

In many ways, these value-defining items function much like the “signature products” I spoke about recently. Every retailer needs products that tell customers, “This store offers good value.” But increasingly, retailers also need SKUs that signify, “This is why you should shop here instead of somewhere else.“

One establishes trust, the other establishes loyalty.

A gallon of milk can help define a retailer’s price image. An Internet-famous chicken preparation, bakery item, prepared meal, or private-label favorite can help define its identity. The strongest retailers understand that these two functions are interconnected. Price image gets shoppers through the door; differentiation gives ‘em a reason to come back.

McKinsey’s bigger, more important conclusion is that grocery competition is shifting from individual tactics to interconnected systems. Value, loyalty, promotions, private label, and fresh departments are coming to reinforce one another as opposed to operating independently.

Consumers, meanwhile, are still assembling their impressions from a handful of products, a series of experiences, and – for good or ill – a small number of memorable moments.